Every category is still in the green! This month I bought IUSN for the first time which means I now own the three ETFs I talk about in my ETF portfolio post. I’m still thinking about whether IUSN should be 10% of my ETF portfolio or if I should rather go for around 5%. Right now I prefer 10%.

Keep in mind my P2P lending portfolio (if you can still call it a portfolio) still shows a positive result. At the moment I only have loans from two companies left. Both companies are enduring some problems at the moment so it could take some time before I get my money back, if at all. I’ve made a small update on my P2P lending portfolio here.

Hi

Just wondering, how do you keep track of your portfolio? Just a spreadsheet you update monthly?

Ik started using a spreadsheet too, but it’s pretty static and annoying to update. Wish my banks & broker had an API which I could connect to an app (with Bitcoin portfolio included). Would be nice ?

Hi Vincent,

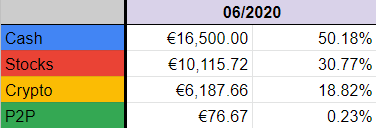

Sorry for this kind of late answer. I was in the Ardennes for the weekend. I use a Google Sheets spreadsheet indeed (you can check it out here).

It keeps track of the current prices automatically via google finance (built-in) formulas, even for my cryptocurrencies (except XRP). I do have to put in my buys myself, but I don’t really mind. I also have tabs for every half-year. This way I can track whether I follow my budgets and project into the future as well.

I’m not completely happy with it, but it is doing the job right now. 🙂

Michiel

Nice ik ga dat schaamteloos kopiëren ?

No problemo, ga je gang! 😀

Done, looks a lot better than my spreadsheet ?

I put my pension fund under stocks, but there’s no google finance integration for ARPE I guess + it’s too complex to calculate what I invested every year so far + tax reduction etc.

Doe jij niet aan pensioensparen? Of zie je je stocks als je eigen pensioenspaarfonds?

Hi Vincent,

Certainly not every fund/stock works with Google Finance, unfortunately!

I looked into ‘pensioensparen’ myself a while ago with my bank (BNP Paribas Fortis). Their funds had high entry- and yearly fees. Together with the 8% (?) you have to pay in taxes when you turn 60 (?) I found out that I would pay more in fees over the years than I got back from taxes yearly. You also don’t have the freedom to access the money when you would want to (or you pay a lot of taxes).

That being said, there are a lot of cheaper options out there that are probably worth it, certainly when you would invest the tax benefit that you get from ‘pensioensparen’. I would like to own my own pension account with the same rules and regulations but with the freedom to invest in what I want. But I don’t think there is a real option to do that?

I should do some more research when I find the time!

Michiel

You might be right. I believed the bank and the government when I started my pension fund. When I look at it that way I feel like an idiot ? Never heard of trackers back then.

Hi Michiel,

Where do you buy EMIM & IUSN shares to reduce the costs? At this moment I’m only active on Degiro. IWDA is in the ‘kernselectie’ of Degiro, the other 2 ETF’s have a higher cost to buy on their platform.

Also I like to know how you the ratio for your 3 ETF’s besides the geographic spreading as I find different ratio’s online for this combination.. (75-12.5-12.5), (70-20-10),..

Keep up the good work with your blog posts! ??

Hello CoppiePaste,

I buy EMIM and IUSN on Degiro as well. I have another post about the ETF portfolio I want to go for. There, I talk about 75-20-5. It this point in time I want to go for 70-20-10.

Because of these smaller allocations I’m only buying EMIM around 2-3 times a year and IUSN around 1-2 times a year. This means that it won’t cost me that much. The fees are not that high anyways!

Thanks for your comment, I hope this answered your question. Sorry if my reply contains some mistakes, I’m answering from my phone 🙂

Kind regards,

Michiel