Let’s take a look at the difference between accumulating and distributing ETFs together with the advantages and disadvantages of each. Deciding which one you should pick will depend on your own preference but it is very likely that the tax situation in your country will have a high impact on the decision-making process. Let’s understand why!

Accumulating ETFs

You should be able to recognize accumulating ETFs when the name of the fund ends with “(acc)”. In the case of accumulating ETFs, dividends that are paid out by the companies which make up the ETF are reinvested automatically by the fund manager. In conclusion, they will never be credited to your account but instead, the fund size will grow which will make your ETF shares more valuable. You will not notice when the dividends are reinvested, because this happens throughout the whole year. When you take a look at the long-term increase in share prices you can see the difference between accumulating and distributing ETFs very clearly. Comparing charts will be shown at the end of the post if you are interested! If you want to know the actual dividend yield of an accumulating ETF you can always check the yield of the distributing counterpart.

This means that you never have to think about reinvesting the dividends yourself. Even more important, in a lot of European countries dividends are taxed higher than capital gains. In my country, Belgium, dividends are taxed at 30% but we don’t have to pay capital gains. This means that investing in accumulating ETFs is very beneficial tax-wise and if you take a look at the ETF portfolio that I am going for you can see that I only want to buy accumulating ETFs.

Distributing ETFs

By now this could already be very obvious. Distributing ETFs distribute the dividends that the underlying stocks pay out. Distributing ETFs can be recognized by ending with “(dist)”. In this case, dividends will be credited to your account in cash, in a lot of countries, this is a taxable event. If you want to create some passive cash flow this could be an option for you. Do take into account that selling some shares from time to time with an accumulating ETF should have the same effect as getting dividends and could be tax beneficial. However, this is research you can only do yourself since it is country-specific.

Comparison

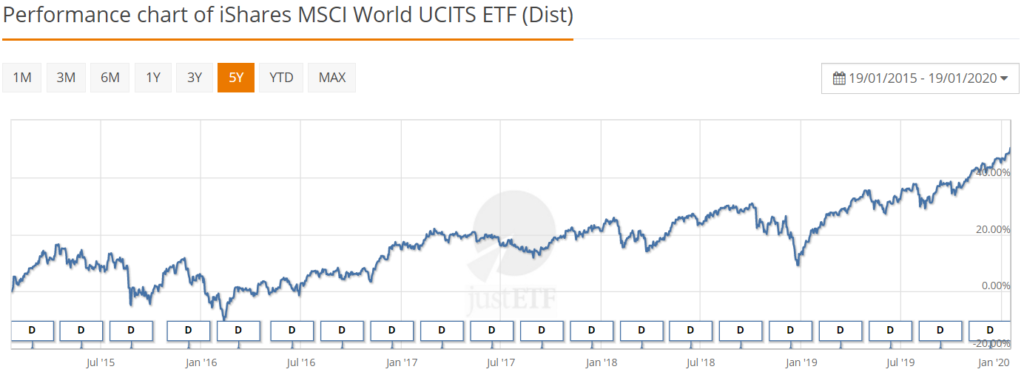

This is the 5-year return chart of IWDA. This ETF tracks the MSCI World index. IWDA is an accumulating ETF. The total 5-year return on the share price was around 66%.

This is the 5-year return chart of an ETF that tracks the same MSCI World index. The only difference is that this is a distributing ETF. The total 5-year return on the share price was around 50%.

As you can see the reinvested dividends are clearly noticeable in the returns over time. Of course, if you take the return of the distributing ETF including dividends, you would have gained roughly the same amount. (but in my case I would have paid taxes!)

Hopefully, now you understand the difference between accumulating and distributing ETFs. The graphs are from a website called JustETF. If you have any more questions don’t hesitate to ask!

Impressive! Thanks for the post.

Best regards,

Boswell Raahauge

Thankyou for the post. Very helpful.

For the case of Belgium, so by investing in accumulating ETFS you dont have to pay any taxes on gains?

For example, if I invest through Degiro broker in accumulating ETFs, I dont need to pay any additional taxes on returns?

I am from Belgium (beginner invester), thats why asking.

tnx to let me know

Hello Ali,

Thanks for the comment. In Belgium, we don’t pay capital gains tax at all. Doesn’t matter if you buy accumulating or distributing ETF (or even single companies). We do pay taxes on dividends though. This is where we can find a difference between distributing and accumulating ETFs. When an ETF distributes its dividends we pay 30% taxes. This is not the case with accumulating ETFs because the dividend never reaches our brokerage account. Instead, it is reinvested by the fund itself.

I hope this makes it a little bit clearer?

Michiel

Thanks Michiel. Its clear.

Hi there, I was comparing the price performance of IWDA Vs IWRD but it seems that IWRD constantly outperform IWDA, I did this comparison on Google charts so isn’t distributing better even without dividend? Comparing a 5 y performance as of 04/06/20 IWRD recorded a 55.9% increase while IWDA recorded a 38.87% increase

Hello James,

Thank you for your comment. I think your information is not correct. I’ve compared the 2 ETFs using ‘justETF’ (good website for finding out ETF information). Here, IWDA outperforms IWRD (including dividends) a little bit over the last 5 years. IWRD also has a higher TER (yearly cost) and the fund size is smaller as well. I’d still prefer IWDA!

Have a great day!

Michiel

Hi Michiel

Beginning invester from Ghent here. I opened an account with Bolero end February this year and my plan is to DCA on VWCE. Since VWCE is on the German stock exchange, it costs € 15 for every buy. I plan to buy every 3 months to lower this cost.

What’s your opinion on VWCE?

Best regards

Vincent

Hi Vincent,

VWCE is definitely a good simple way to go. You don’t need anything else really. This way you don’t overcomplicate things at all.

€15 for every buy is definitely a steep price. Except if you are buying thousands of euro at a time (but even then). Bolero will probably not be a bad broker (from KBC if I’m not mistaking?) but maybe take a look at cheaper options like Degiro!

Anyway, if you are going to stick with bolero make sure you save up enough before buying. Even if you buy €1000 each time, you are still paying 1.5% in fees every buy which is quite a lot in my opinion!

I hope this answers your question!

Kind regards,

Michiel

I thought, probably wrong, that there were drawbacks to a foreign broker, which is why I went for Bolero. At that time I also did not know that VWCE existed, I was planning on buying VWRL.

Hello Vincent,

There are no drawbacks to using Degiro. They even withhold Belgian taxes automatically, so you don’t have to worry about that either. Either way, Bolero is probably not a bad broker. Just not the cheapest one (by a long way).

Kind regards,

Michiel

Something that just now occurred to me: maybe I should follow the same advise I took to heart for my pension funds and invest just once a year in January (https://www.tijd.be/netto/pensioen/storten-in-januari-levert-een-grotere-pensioenspaarpot-op/10086828.html). That way the additional cost of the German stock exchange less important. What’s your take on that idea? Or is the opportunity cost at play (because my money is sitting idle on the bank)?

Hi Vincent,

I did a quick diagonal read of the article. It makes sense that if you save ~€1000/year into a pension fund, you will most likely have better returns if you just invest the whole sum in January (this means that your money is invested for a longer time).

I try to invest €1000/month in ETFs, so around €12.000/year. I don’t have this €12.000 all ready in January to invest at the same time. So instead, what you will be doing is keep your money out of the market for 12 months to invest it all at once. This is the opposite of what the article is about. There you invest your money for the whole COMMING year in January. If you wait 12 months to invest you will be investing the money of LAST year.

I hope this explanation makes sense? Like you said, keeping your money in the bank means you are missing out. If you stick with Bolero, you’ll have to find to balance between getting your money into the markets as fast as possible and paying as less fees as possible.

Kind regards,

Michiel

Great reply, thanks for your insight!

Hi Michiel, your stalker again ?

Probably a stupid question, but how can you tell that your portfolio of accumulating ETF is gaining in value? When I multiply the amount of VWCE I bought with the current price I get the exact value of my portfolio. I thought the value of your portfolio would increase independent of the current price of the ETF somehow?

Hi Vincent,

Nope, the value of your portfolio is always equal to the number of shares * share price. Maybe I am not understanding fully what your question is about, but it could be that you don’t completely get the concept of accumulating ETFs?

ETFs are a basket of stocks and some of these stocks return dividends to their shareholders. In this case, the company that manages the ETF receives the dividend. Now, they can do two things with this dividend. They can return it to the shareholders of the ETF in cash, or they can buy new company shares. In the case of accumulating ETFs, new company shares are bought. This means that the underlying value of the ETF goes up after which the share price should increase as well!

Thus, if the share price increase, your portfolio value is still ‘Amount of shares * share price’!

Does this answer your question? If not, don’t hesitate to clear things out!

Michiel

I’m very new to this, so you’re absolutely right that I don’t grasp the concept of accumulation.

So, the price increase of a share in VWCE increases based on 2 things: the market (people buying or selling shares) AND dividends that are used by vanguard to buy more company shares for VWCE.

Does this mean that the price of a share of VWCE will eventually exceed the price of VWRL, because not everyone buys more shares of VWRL with their dividends?

Hi Vincent,

You are almost there! In fact the share price only depends on people buying and selling the shares. But the share price will always (closely) represend the underlying value. If the ETF share price is lower than the underlying stocks it represents, people can buy at a ‘discount’ which will cause the price to go up. This is also true the other way around. So, this does mean that when the management company buys new shares with the dividends, the share price will go up because people are willing to pay more, because it is worth more! Does this make sense? 🙂

As you can see in the comparison above, the accumulating ETF’s share price will have a better return. So, this should mean that VWCE will indeed eventually surpass VWRL!

Michiel

Can’t say I fully grasp it, but it clearer now anyway. Thanks for that. What I don’t understand yet is the underlying value. VWCE has like 3.000 + companies, nobody knows the true underlying value do they? Nobody knows how the stock markets move (man and dog reference, where stock market is the dog and man the economy)? You buy and hope it will go up (eventually), magically somehow.

Hi Vincent,

Actually, it is not that difficult to know what the value of an ETF is (at a certain point in time). Let’s say an ETF invests in 3 companies, A, B and C. The ETF owns 1 share of each company. One share of company A is worth €700, one share of company B is worth €200 and one share of company C is worth €100. This means that the value of the ETF is a total of €1000.

Let’s say the ETF issued 10 shares. This means each share of the ETF is worth €100. The actual share price of the ETF will most likely be very close to this €100 as well. If it would be €95, people can actually buy company A, B and C at a discount. Discounts will probably be quickly bought by investors because they can now buy something that is worth €100 for less, which will cause the price to go back up and vise versa.

Let’s say the ETF receives €100 in dividends. It is an accumulating ETF, so it will buy more shares. Now the value of the ETF is €1100 which will cause the price of each individual share to be around €110 as well.

This is the best I can do 😀 I hope you get it a little bit more now! 🙂

Michiel

Maybe it’s easy for you ? VWCE, like VWRL, invests in 3421 companies (percentages). I can’t find anywhere how many shares are issued. But even when I did, I’d need a very large dynamic spreadsheet to keep track of the actual value of the shares of all those companies by percentage.

Maybe professional investors have tools to keep track of this to know when an index fund ETF is undervalued, but I doubt investors like that are interested in trackers like VWRL. S&P500, maybe, but all world trackers with a spread as large as VWRL seem to be something for the not so professional (active), not so all knowing investor.

But I’m probably wrong, or only half right ?

Hi Vincent,

I don’t think you need to be really concerned about whether an ETF is discounted or not. Since it is an open market it should be balanced all the time. You can actually look up the premium/discount on some websites. This one has it for example!

But like I said before don’t get hung up on this. In my opinion, passive ETF investing is the way to go. Just buy weekly/monthly/quarterly, do this for as long as you can and you will most likely be better off at the end!

Michiel

Hi Michiel,

Firsr of all, congratulations on your website. It is very easy to read. I came across your website searching about the difference between Accumulating Vs Distributing ETFs. This because of the way dividends are taxed in Belgium. And to my surprise after reading more I quickly realised you are from Belgium too. Beginner investor here.

What made you pick the IWDA ETF ? Any advantages picking this one vs VWCE? I don’t see a lot of differences besides the inclusion of emerging markets in the VWCE?

Thanks, looking forward to more posts 🙂

Hi Dany,

Sorry for the late answer, I was enjoying some holidays!

VWCE is certainly not a bad choice! I like the freedom to tweak the allocation I want to give to emerging markets, this is why I didn’t go with VWCE. VWCE also has a TER that is a bit higher than IWDA and EMIM combined, but this is a difference you won’t really notice.

If you like VWCE, go for it! 🙂

Kind regards,

Michiel

Hi Michiel,

first thx for all the info :), im a new invester from israel and im trading with IB broker so i can trade somewhat cheeply in the NYTE (in israel it quiet expansive..).

any way, i want to invest for long time (30+ years) and i discover that with dividend investing i got 47.5% tax in total! (30% from usa + 25% from israel). so the accumulating index etf, as i see it, is the way to go for me but the problem is that i have not found any accumulating ETF in the NYSE (for S&P\QQQ\DOW etc..), can you please tell me how can i find those type of etf? where sould i look for them?

Shai,

Hi Shai,

Thank you for your comment. Accumulating ETFs do not exist in the US. This is why you are not able to find them. JustETF has a research tool where you can apply your criteria to find ETFs you are interested in!

I hope this answers your question?

Kind regards,

Michiel

Hi Michel.

Nice article. Thanks.

You stated back in April: “In Belgium, we don’t pay capital gains tax at all.”

I think we need to make a distinction for accumulating funds containing more than 10% of assets in fixed interest securities. These funds are subject to 30% tax (Reynders-tax) on the capital gain of the fixed interest component of the fund upon sale.

I currently do a few quick calculations when deciding for accumulating versus distributing EFTs, taking into account for example, %bond component, historical dividends paid for DIST version (not that there is a guarantee the trend will continue), …

What are your thoughts?

Thanks.

All the best, Colin

Hi Colin,

I should have mentioned that I was talking about equities only, you are correct. I am a firm believer that a portfolio of 100% equities is a good move when you are still young. With ‘young’ I mean not close to retirement. I will only start thinking about fixed income securities once I want to rely on my investments to live off.

I do have to be honest here and tell you that for this reason, I haven’t done much research yet on adding fixed interest securities to my portfolio. If you have found the most optimal way of adding bonds to your portfolio in Belgium, please let me know! With you asking me about it, my interest is piqued though. If I find the time, I’ll take a closer look at it as well.

I am sorry that I could not be of more help to you..

Kind regards,

Michiel

Thanks for your quick reply Michiel.

I use a few bond funds – Government Gilts (I’m older 🙂

I try to keep them separate from my other EFTs (ie, like you, I aim for 100% equities in my other EFTs).

Enjoy “the journey”.

Hi Colin,

Thanks for the comments, I always like communicating with other investors!

Enjoy your investment journey as well!

Kind regards,

Michiel

Hello and many thanks for your work on your site! It’s been of tremendous help!

Could I bother you with a question?

What is your opinion on the “vanguard all world high dividend accumulating”? Is it likely to gain high value over the years? Since it offers a lot of dividends that are being reinvested. Does it sound promising for a passive investor and for the long run?

Many thanks again and kind regards

Christos

Hi Christos,

Sorry for the late reply. To start with my answer: this is probably not a bad fund. That being said, all the companies in this fund are most likely also in ETFs like VWCE and IWDA. These have actually even performed better than “vanguard all world high dividend accumulating” and have a lower TER as well. I would always prefer IWDA or VWCE but it is your choice of course! 🙂

Kind regards

Thank you for your reply! Did some more research.. you are absolutely right! 96% of its companies are in vwce! I will stick with vwce as it is my personal favourite. Cheers!